Many people we speak to see budgeting as a necessary evil to make their money work. Others see it as a complicated process that's not worth their time. There are many who would like to budget more but don't know where to start.

We truly believe that budgeting is for everyone because it can achieve different things for different people. Whether you're looking to plan for the future, go on that dreamy holiday, increase your savings or simply make your money work - budgeting will help you do all of that. What's best: with a structured process and a bit of discipline it doesn't have to be difficult.

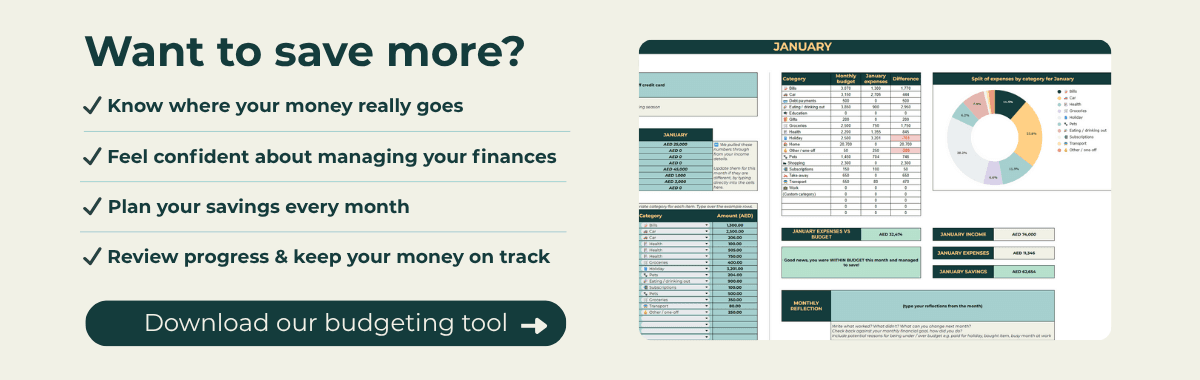

Our simple 5-step approach guides you through understanding your income, setting up a budget and tracking your progress. You can use our free budgeting tool to navigate this journey with ease.

Where possible we recommend you follow this process at a household level, i.e. combined income and expenses across your family, though you can still track personal spending within that. This will give you a holistic view and bring out the most value. Let's dive into the steps.

1. Understanding your income

This should cover all your income sources across the household. Salaries are usually the key component but don't forget to add in any rental or investment income you receive on a regular basis. Bonuses should also be worked into the annual view but make sure you don't account for them too early in your spending.

2. Setting your budget

Now that you understand your income, it's time to look at your spending. The goal here is to structure your outgoings in a reasonably predictable way every month. A good starting point is the 50/30/20 rule, which - as a rough guideline - says you should split your income in the following way:

- 50% Needs: Necessities - things you have to pay for every month, such as rent, mortgage repayments, school fees, kids clubs, car loan repayments, food shop, necessary clothing, etc.

- 30% Wants: Your lifestyle choices - date nights, dinners with friends, nights out, pool days & brunches, aqua parks with the kids, the new outfit you want. The budget will only work if it makes you happy, so this 30% is important!

- 20% Savings: Planning for the big things - retirement, sending children to university, an upgrade on the car or that big holiday you've been dreaming of.

One good way to start is to look at the last three months' expenses and base your budget on that. See how it compares against the 50/30/20 rule and check where you can optimise.

Sometimes immediate changes to your expenses can't be made and that's ok! Make sure you have a target budget that you are actively working towards and track that progress.

3. Emergency fund

Setting up an emergency fund should be your first savings goal if you don't already have one. The purpose of the fund is to tide you over should the unexpected happen - sudden job loss, health problems, or anything that would reduce your expected income.

This fund buys you time to get your life back on track and should cover 6 months' worth of "Needs" expenses and, ideally, some of the "Wants" expenses to allow for some level of normality when things don't go to plan.

It's important to focus on that, as it provides you with stability and will make you feel better about your finances.

Get the next UAE money briefing in your inbox.

Join the readers getting practical UAE money updates, not generic personal-finance filler.

4. Paying yourself first - the best way to save

Setting up your budget upfront allows you to know how much you can save each month. Yet so many of us only save what's left at the end of the month - which 9 times out of 10 will be less than we budgeted.

That's because keeping the money in your account provides you with false "spending power" at the expense of your bigger savings goals.

So do yourself a favour and pay yourself first! When you get your income, transfer the savings portion into your savings account and keep it there (and don't worry, you can take it out again if you really need to!).

5. Tracking & self-reflection

You won't know how well you're doing unless you track your results. Initially, you should look at your budget on a monthly basis, record your expenditures and see where you can improve or adjust your budget. Over time, you'll get a good feel for where you are and be able to go down to quarterly reviews.

Reflecting on your journey can give you a sense of achievement, motivate you and highlight areas where you can do better. And don't forget to be proud of your successes, no matter how small they are!

As mentioned upfront, this journey is easier with our free UAE budgeting tool (or other tools you may prefer), so go ahead and have a glance over it! It may inspire you to start.